June Week 4 Market Brief

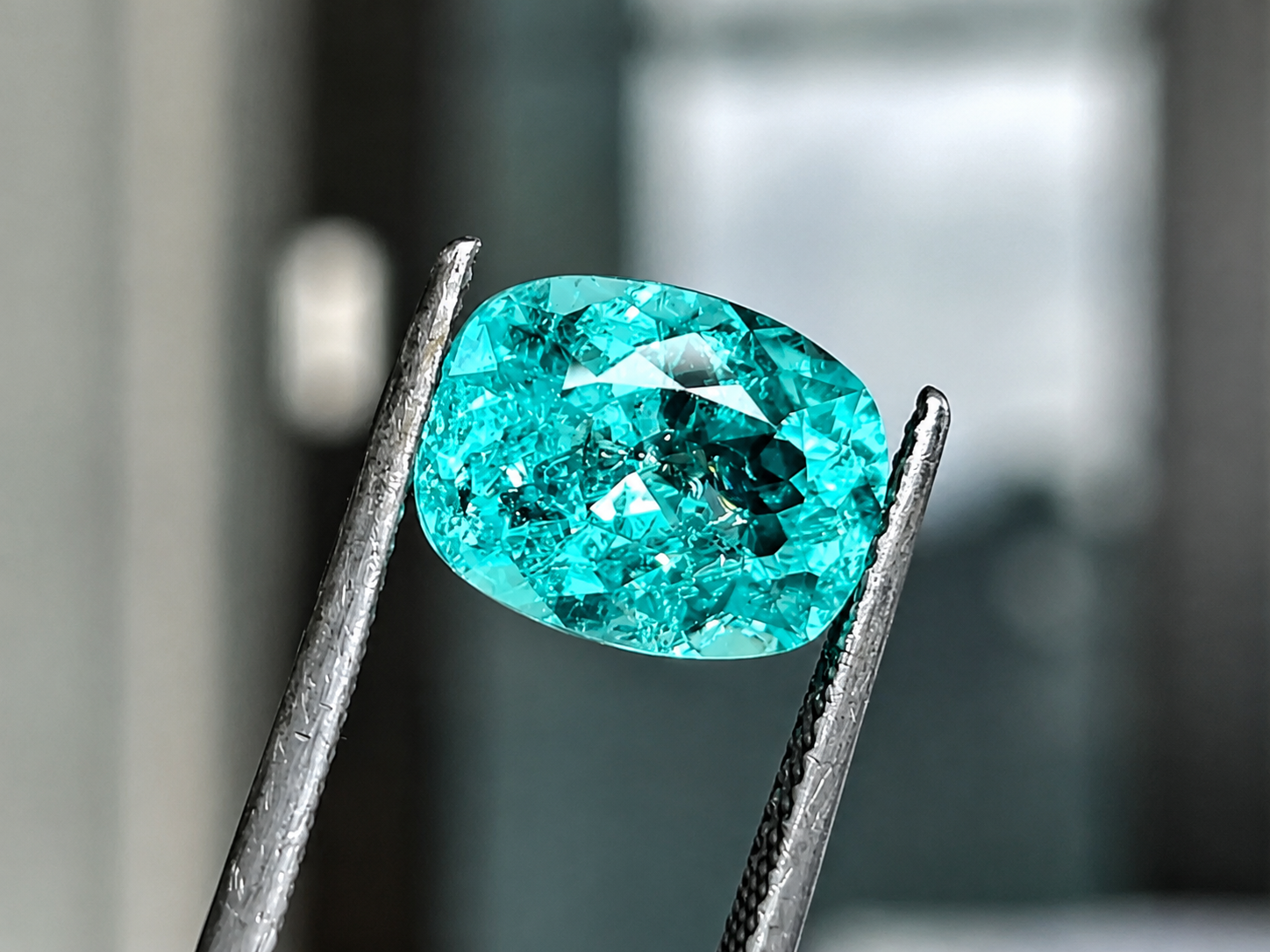

Paraiba Tourmaline, Image courtesy of Geology Science

Market Snapshot

The Gemological Institute (Gemworld International) announced on 17 June 2026 that its forthcoming July and August issue of The GemGuide, the colored stone trade's principal B2B pricing reference, will reduce its grading scale for unenhanced Burmese ruby from ten grades to four, citing the inability to source sufficient fine material to price across the previous range confidently. At the same time, it materially increased its pricing guidance for Mozambique ruby, with Research Director Stuart Robertson stating that prices had "skyrocketed" and noting that major luxury brands have become significant buyers of Mozambique production, often paying premiums to secure reliable inventory. This is not simply a revision of price tables. It is an acknowledgement that the traditional assumptions underpinning the valuation of colored stones no longer reflect the market. Premium natural material is becoming sufficiently scarce that continuous price discovery is no longer possible across historical quality bands, while branded buyers are increasingly absorbing top-tier supply before it reaches the broader dealer market.

That structural repricing is simultaneously increasing the value of trust. On 15 June 2026, the Swiss Gemmological Institute issued a trade alert warning that emeralds are being chemically cleaned, submitted for laboratory examination in their untreated state, certified as showing no clarity modification, and subsequently refilled with oil or artificial resin before being sold using the original report. The institute confirmed that the practice has resurfaced in recent months and extends beyond emeralds to any gemstone with fillable fissures, including ruby. As the premium for documented, minimally treated stones widens, the financial incentive to manufacture credibility widens alongside it. Certification is therefore no longer merely evidence of quality. It is increasingly becoming part of the scarce asset itself.

The market is already reflecting that shift. Sotheby's Magnificent Jewels sale in New York demonstrated that professional pre sale estimates based on recent comparable transactions are struggling to keep pace with current demand for exceptional colored stones. A 6.11 carat Brazilian Paraíba tourmaline sold for $972,800 against a high estimate of $500,000, while a 7.70 carat Paraíba realized $1.4 million against a high estimate of $800,000. A 1970s Van Cleef & Arpels ruby, emerald and diamond sautoir achieved $345,600 against a high estimate of $80,000. When specialist auction houses consistently underestimate final prices by such margins, it suggests that the premium segment is repricing faster than established valuation models can adjust.

The demand side of the same restructuring appeared at Jewellery & Gem ASIA Hong Kong, which concluded on 21 June with nearly 24,000 unique buyers across approximately 1,100 exhibitors. While Chinese attendance softened modestly amid weaker domestic economic conditions, organizer Informa Markets reported "fewer but more meaningful interactions," with buyers arriving to execute targeted sourcing strategies rather than browse inventory. Attendance from Cambodia increased 52%, Thailand 6%, the Philippines 5.6%, and India 2.16%, indicating that regional demand is becoming more diversified even as purchasing behavior grows increasingly selective. Taken together, the week's developments point to a single structural conclusion: the colored stone market is no longer rewarding volume alone. It is increasingly rewarding scarcity, provenance, documentation, and quality, while disciplined buyers compete more aggressively for exceptional material and apply greater scrutiny to everything else.

What This Means For Zambian Miners

This week's developments point to a structural change in where value is being created across the colored stone supply chain. The market is no longer paying solely for the geological quality of a stone. It is increasingly paying for confidence in that stone's origin, treatment history, documentation, and long term collectability. GemGuide's decision to restructure its ruby pricing methodology confirms that premium material has become sufficiently scarce that historical pricing models can no longer describe the market with precision. The Swiss Gemmological Institute's fraud alert demonstrates that documentation itself has become valuable enough to counterfeit, while Sotheby's results show that buyers continue to pay substantial premiums for exceptional stones with trusted provenance despite broader economic uncertainty.

For Zambian miners, this shifts the competitive advantage away from production volume and toward inventory quality and presentation. A miner producing fewer, well sorted, well documented stones is increasingly positioned to outperform one selling larger mixed parcels into the commercial market. Premium emeralds displaying strong color, good transparency, and minimal treatment should be separated immediately at the point of recovery, retained in homogeneous parcels, and accompanied by clear records of origin wherever possible. As buyers become more selective, the discount applied to mixed quality parcels is likely to widen, while well presented premium material should continue attracting stronger competition.

The commercial implications extend beyond individual sales. Buyers attending Jewellery and Gem ASIA Hong Kong reported fewer but more purposeful purchasing decisions, indicating that transactions are becoming increasingly planned rather than opportunistic. This favors miners who can offer consistency, repeatability, and confidence over those relying on one off negotiations. Building a reputation for reliable grading, transparent disclosure, and consistent parcel quality is becoming a commercial asset capable of generating pricing power beyond the intrinsic value of the stones themselves.

The current environment therefore rewards discipline rather than urgency. Continue presenting premium material into higher quality buying windows where international demand has remained resilient, while resisting the temptation to combine exceptional stones with commercial production for faster liquidity. The market is increasingly distinguishing between ordinary supply and trusted supply, and that distinction is likely to become one of the most important drivers of pricing through the remainder of 2026.

Export & Compliance Update

Commercial shipping through the Strait of Hormuz has begun recovering following the reopening agreement reached earlier this month, although traffic remains well below pre conflict levels and freight markets have yet to normalize. Vessel movements have increased steadily over the past week, reducing the immediate risk of prolonged supply disruption, but insurers continue to apply elevated war risk premiums and logistics providers have not materially reduced transport pricing into Asia.

For gemstone exporters, the practical guidance remains largely unchanged. Continue budgeting for higher than normal freight costs and longer delivery timelines, while avoiding assumptions that shipping rates will return quickly to pre conflict levels. The immediate crisis has eased, but the cost environment has not. Export planning should therefore continue using the conservative assumptions adopted in the previous brief until sustained improvements in freight pricing and shipping capacity become evident.

Opportunity of the Week

The strongest commercial opportunity this week is not a particular gemstone but a stronger market position. As buyers become increasingly selective and confidence becomes a larger component of pricing, miners who consistently present reliable information alongside their stones are beginning to distinguish themselves from equally qualified competitors. A miner able to describe where a stone was recovered, how it has been handled, and whether any treatment has occurred is increasingly offering something the market values beyond the stone itself. For premium emeralds, that additional confidence may become the deciding factor between competing buyers, particularly as international dealers and luxury brands continue prioritizing transparent sourcing.

SAVVY continues to actively purchase premium, high quality, and good quality rough material for established Chinese buyers, with particular interest in well presented parcels supported by transparent origin information and stones suitable for laboratory certification.

Practical Tip

When presenting stones to a buyer, spend as much attention on the parcel as the gemstones themselves. Keep each parcel consistent in quality, clearly identify the mine or recovery area where possible, disclose any known treatments from the outset, and prepare a simple written description before negotiations begin. Buyers making increasingly selective purchasing decisions often compare several parcels in a single day, and a miner who presents organized, transparent information can create confidence before price discussions even begin. As the market continues rewarding trusted supply, professionalism itself is becoming a competitive advantage.

Closing

We continue to provide gemstone and jewelry market intelligence relevant to the Zambian gemstone mining and trading industry, with the goal of improving information flow, market understanding, and trade facilitation.

This briefing will be published every Friday.